When selling a business, one of the most important decisions you will make is how the transaction is structured. Most deals fall into one of two categories: an asset sale or a stock sale. While both result in a transfer of ownership, the financial impact, legal obligations, tax consequences, and overall deal strategy can differ drastically between the two.

For many business owners, the distinction isn’t immediately clear — but it determines everything from how much money you walk away with to how much risk the buyer assumes after closing. Buyers and sellers often prefer opposite deal structures because each carries unique benefits and drawbacks. That’s why understanding these structures early can prevent costly mistakes and give you a stronger negotiating position.

From a business broker’s perspective, the way a deal is structured is not an afterthought; it’s a core part of valuation, tax planning, due diligence, and negotiation. It can influence:

- Seller’s payout after taxes

- Buyer’s future depreciation benefits

- Transfer of contracts, leases, and licenses

- Liability exposure on both sides

- Whether the deal closes smoothly or becomes delayed

I have broken down everything in detail in this guide.

By the end, you’ll understand which structure aligns best with your goals, and how a skilled business broker helps you navigate the complexities so you exit on the strongest possible terms.

What Is an Asset Sale?

An asset sale is the most common way small and mid-sized businesses are bought and sold. In this structure, the buyer purchases specific assets of the company, rather than the company’s shares or legal entity itself. This means the buyer is acquiring the parts that make the business operate — but not the corporate shell.

From a legal and financial standpoint, the seller continues to own the original company entity after closing, while the buyer starts fresh with the assets they’ve acquired. Because of this, asset sales are often seen as “cleaner” and lower-risk transactions for buyers.

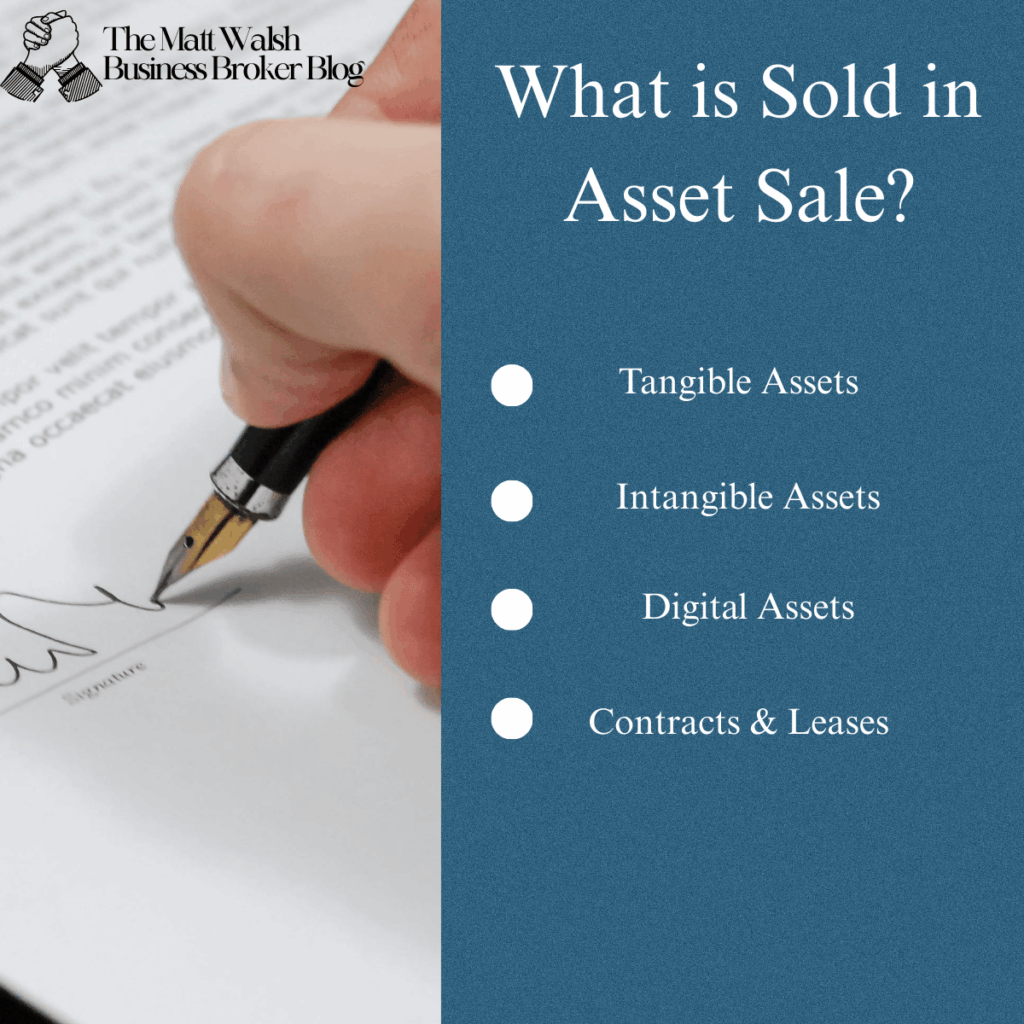

What Exactly Is Purchased in an Asset Sale?

The buyer can selectively acquire the assets they want, such as:

- Tangible assets: equipment, machinery, inventory, vehicles, tools, furniture

- Intangible assets: brand name, trademarks, customer lists, phone numbers, copyrights

- Digital assets: website, domain, social media accounts, online storefronts

- Contracts and leases: sometimes transferable, sometimes requiring third-party consent

Buyers may also choose to leave behind specific assets they don’t want — such as obsolete equipment, excess inventory, or certain liabilities tied to the old entity.

How Liabilities Are Handled

One of the primary reasons buyers prefer asset sales is limited liability exposure.

In most cases:

- Liabilities remain with the seller

- Buyers take on only the obligations they explicitly agree to assume

This removes the risk of inheriting unknown lawsuits, tax issues, debt, or legal claims from the seller’s corporation.

Tax Implications of an Asset Sale

Tax treatment is a major factor in deal structure.

For buyers:

Asset sales are generally advantageous because buyers get a stepped-up basis in the acquired assets.

This means they can depreciate or amortize assets at new, higher values — resulting in substantial future tax deductions.

For sellers:

Asset sales can be less favorable. Certain assets, like inventory or accounts receivable, may trigger ordinary income tax rather than lower long-term capital gains rates.

Additionally, the IRS requires that the buyer and seller allocate the purchase price across various asset classes, and that allocation can significantly affect tax outcomes.

Why Buyers Prefer Asset Sales

Business brokers often see buyers gravitate toward asset deals because they offer:

- Lower risk

- Better tax deductions

- More control over what’s included in the purchase

- A cleaner transfer of the business’s operations

For these reasons, asset sales dominate many small business transactions — especially retail, service, e-commerce, contracting, and manufacturing companies.

What Is a Stock Sale?

A stock sale is the alternative deal structure to an asset sale, and it’s generally favored by sellers — especially in mid-sized businesses or companies with strong long-term contracts, specialized licenses, or complex operational structures. In a stock sale, the buyer purchases the owner’s shares or membership interests, effectively acquiring the entire company as-is.

Instead of picking and choosing assets, the buyer steps into the shoes of the current owner and takes over the business entity in its entirety. The legal corporation, its history, and all of its obligations remain intact — only the ownership changes.

What Transfers in a Stock Sale?

Because the entity stays the same, everything within the business transfers automatically, including:

- All assets (equipment, IP, inventory, digital assets)

- All liabilities (loans, debts, lawsuits, obligations)

- Contracts and leases that belong to the entity

- Employees and payroll accounts

- Licenses, permits, certifications

- Vendor agreements and customer contracts

- Tax ID, EIN, and corporate history

This continuity makes the transition simpler in industries that rely heavily on regulatory approvals or long-term agreements.

Why Sellers Prefer Stock Sales

From a broker’s perspective, sellers almost always prefer stock sales because:

1. Cleaner Tax Outcome

Most sellers pay long-term capital gains tax — which is often much lower than the ordinary income rates triggered in asset sales.

2. Fewer Post-Sale Liabilities

Because the buyer assumes the entity, the seller typically has minimal ongoing obligations once the sale is complete.

3. Simpler Deal Flow

There is no need to reassign assets one-by-one.

Instead, ownership transfers via a single stock or membership interest purchase agreement.

4. No Need to Reapply for Certain Licenses

In industries like:

- Healthcare

- Construction

- Financial services

- Real estate

- Professional services

- Environmental or government contracting

…it is often significantly easier to sell the existing entity rather than move licenses to a new one.

Drawbacks for Buyers

Despite seller advantages, buyers may be hesitant to agree to stock sales because:

- They inherit all historical liabilities, even unknown ones

- There may be unresolved tax or legal issues

- Some lenders prefer asset collateral

- It is harder to walk away from problematic business history

This is why due diligence is typically more thorough and time-consuming for stock transactions.

When Stock Sales Are Most Common

Business brokers see stock sales frequently in:

- SaaS companies with long-term subscription contracts

- Medical or dental practices

- HVAC, plumbing, electrical, and other licensed trades

- Manufacturing firms with vendor certifications

- Defense or government contractors

- Multi-location service businesses

- Anytime licenses are non-transferable

If keeping the corporate identity unchanged is essential, a stock sale often becomes the preferred structure.

What is Section 338(h)(10) and Why it Matters?

Section 338(h)(10) is one of the most misunderstood — yet most powerful — tax tools available during a business sale. It sits at the intersection of asset and stock transactions, allowing buyers and sellers to structure a deal that looks like a stock sale on paper, but is treated as an asset sale for tax purposes.

For many deals, especially mid-market transactions or sales involving S corporations, this election can dramatically improve outcomes for both sides when negotiated strategically.

What Section 338(h)(10) Actually Does

Under normal circumstances:

- A stock sale is taxed like a stock sale.

- An asset sale is taxed like an asset sale.

But Section 338(h)(10) creates a hybrid option:

The buyer purchases the stock of the company.

For tax purposes, the IRS treats the transaction as if the buyer purchased assets instead.

This gives buyers access to the stepped-up basis and depreciation benefits normally available only in asset sales — even though the legal structure remains a stock sale.

Who Can Use a 338(h)(10) Election?

This election is not universal. It’s allowed only in specific situations, such as:

- Sales of S corporations

- Sales of subsidiaries of larger corporations (e.g., via a parent company)

- Transactions where both buyer and seller agree to the election

Notably, LLCs taxed as partnerships cannot use 338(h)(10), and C-corporations have different limitations.

In brokered deals, 338(h)(10) elections are most common when selling tax-efficient S corporation entities.

Why Buyers Love Section 338(h)(10)

Buyers push for this election because it gives them the “best of both worlds”:

1. Stepped-Up Basis on Assets

They can depreciate assets as if they purchased them new — a major long-term tax advantage.

2. Reduced Liability Risk

Although technically a stock sale, buyers receive certain protections similar to an asset deal (depending on how the agreement is drafted).

3. Clean Continuity

All contracts, licenses, and employees remain with the entity — no need to renegotiate or reassign most documents.

Why Sellers Sometimes Agree to It

While 338(h)(10) can increase the seller’s tax burden, there are reasons a seller may still accept:

- Buyers are often willing to pay a higher purchase price to secure the tax benefits.

- The seller may prefer the simplicity of a stock sale — fewer assignments, smoother transition.

- In competitive deals, offering a 338(h)(10) election can make the seller’s business more attractive to buyers.

A business broker will typically model both scenarios (with and without the election) to understand the required price adjustment.

338(h)(10) in Real Brokered Transactions

Business brokers commonly use this tool when:

- Sellers want a stock sale

- Buyers want an asset sale’s tax treatment

- Both want to avoid the administrative burden of reassigning hundreds of contracts

- The business relies heavily on non-transferable licenses or certifications

When executed properly, 338(h)(10) becomes a negotiation lever that brings the two parties to an agreeable middle ground.

Asset Sales vs. Stock Sales

While both structures accomplish the same ultimate goal — transferring ownership of a business — asset sales and stock sales function very differently. Understanding these differences is essential because the structure you choose directly affects your taxes, liabilities, buyer pool, and overall transition experience.

Below is an expert-level comparison from a business broker’s perspective, breaking down the major distinctions that influence negotiations and deal strategy.

Tax Treatment

Asset Sale

- Buyers get a stepped-up basis, allowing them to depreciate assets at current fair market value.

- Sellers may face higher taxes, especially if significant purchase price is allocated to inventory, equipment, or accounts receivable — all of which can trigger ordinary income rates.

Stock Sale

- Sellers typically receive long-term capital gains treatment, which is often more favorable.

- Buyers miss out on stepped-up depreciation unless a 338(h)(10) election is used.

- Tax complexity is lower because the entity itself continues unchanged.

Liability Exposure

Asset Sale (Lower Buyer Risk)

- Buyers do not inherit historical liabilities unless they explicitly agree to assume them.

- Most past legal, financial, or tax issues remain with the seller’s entity.

- Buyers essentially get a clean slate.

Stock Sale (Higher Buyer Risk)

- Buyers acquire the entire entity — debts, obligations, lawsuits, unknown risks included.

- This requires deeper due diligence and often more legal protections in the purchase agreement.

Deal Complexity

Asset Sale

- Requires assigning or transferring each asset individually.

- Contracts may require third-party consent.

- New bank accounts, payroll accounts, tax IDs, and vendor setups are needed.

- More administrative work on both sides.

Stock Sale

- Much simpler operationally.

- The entity stays intact — same EIN, same bank accounts, same licenses.

- Fewer moving parts, faster transition.

Bottom line:

Stock sales are generally smoother for day-to-day continuity.

Assignment of Contracts and Leases

Asset Sale

- Many contracts (especially leases, vendor agreements, and licensing) require landlord or supplier approval before assignment.

- In regulated industries, contracts may not be transferable at all.

Stock Sale

- No assignment required because the entity holding those agreements is unchanged.

- This makes stock sales ideal for businesses reliant on:

- Long-term service contracts

- Government contracts

- Controlled licenses (healthcare, trades, financial services)

- Long-term service contracts

Financing & Valuation Impact

Asset Sale

- Some lenders prefer asset deals because assets provide collateral.

- SBA financing often aligns well with asset purchases (though both structures are eligible).

Stock Sale

- Buyers may have fewer collateral options.

- Lenders may require stronger guarantees or additional diligence.

Regulatory & Licensing Issues

Asset Sale

- May require reapplication for state licenses, franchise approvals, permits, or certifications.

- In industries like medical, HVAC, daycare, or financial services, this can delay closing.

Stock Sale

- Avoids reapplication because the licensed entity stays the same.

- Smoothest path for regulated or compliance-heavy industries.

Which Is Better: Asset Sale vs Stock Sale?

In my experience, I have seen business owners struggle with this question.

Choosing between an asset sale and a stock sale is not a one-size-fits-all decision.

After all, both of them have their pros and cons.

Each structure favors different goals, tax profiles, and risk tolerances. What’s “better” ultimately depends on whether you are the buyer, the seller, and the type of business being transferred. As a business broker, this is one of the first discussions we have with clients because it directly affects net proceeds, deal timeline, and closing certainty.

I have broken down their qualities:

It Depends on Buyer vs. Seller Objectives

When Asset Sales Are Better

Asset sales tend to favor buyers because they offer:

- A clean slate with minimal inherited liabilities

- Ability to depreciate assets at stepped-up values

- Flexibility to exclude unwanted assets or obligations

- Easier financing in certain industries

Asset sales are also ideal for:

- Retail, e-commerce, and service businesses

- Manufacturing and equipment-heavy operations

- Businesses with no major regulatory or licensing restrictions

When Stock Sales Are Better

Stock sales are more advantageous for sellers, particularly because they often qualify for long-term capital gains tax, which can significantly reduce the seller’s tax bill.

Stock sales are also preferred when:

- The business holds non-transferable licenses (medical, financial, trades)

- The company has numerous long-term contracts that would be difficult to reassign

- Maintaining the operational continuity of the entity is critical

- The seller wants a simpler exit with fewer post-closing obligations

Which Structure Maximizes the Seller’s Net Proceeds?

Most sellers find they walk away with more money through a stock sale because of capital gains tax treatment. In an asset sale, a larger portion of the purchase price may be allocated to ordinary income categories, often resulting in a higher tax burden.

However — and this is where strategic negotiation comes in — buyers may be willing to pay a higher purchase price in an asset sale due to the tax advantages and reduced liabilities. A broker will model both scenarios to determine which structure produces the highest net benefit after taxes.

What About Hybrid Structures?

A 338(h)(10) election creates a hybrid solution when:

- The seller wants the simplicity of a stock sale

- The buyer wants the tax advantages of an asset sale

This option can bridge the gap, but it requires careful CPA involvement and mutual agreement.

Asset Sale vs. Stock Sale: Comparison Table

| Category | Asset Sale | Stock Sale |

| What Is Purchased? | Buyer purchases specific assets (equipment, inventory, IP, contracts, etc.) | Buyer purchases the seller’s shares or membership interests, acquiring the entire entity |

| Ownership of Entity | Seller keeps the legal entity | Buyer acquires the legal entity “as-is” |

| Liabilities | Typically remain with the seller unless specifically assumed | Buyer inherits all known and unknown liabilities |

| Tax Treatment (Seller) | Often worse for seller; part of purchase price may be taxed as ordinary income | Usually more favorable; taxed as long-term capital gains |

| Tax Treatment (Buyer) | Buyer receives stepped-up basis and better depreciation benefits | No stepped-up basis unless 338(h)(10) election is used |

| Contracts & Leases | Many require landlord/vendor approval; some are non-transferable | Usually remain in place automatically because the entity doesn’t change |

| Licenses & Permits | Must often be re-applied for; can delay closing | Stay intact since entity continues unchanged |

| Risk Exposure (Buyer) | Lower risk — buyer avoids historical issues of seller’s entity | Higher risk — buyer assumes all past liabilities and compliance obligations |

| Deal Complexity | More complex; asset-by-asset transfer; multiple assignments required | Operationally simpler; entity continues smoothly with new owner |

| Financing | Often easier to finance, especially with SBA lenders | Sometimes more difficult due to collateral limitations |

| Best For | Buyers, asset-heavy businesses, companies with minimal contracts or regulations | Sellers, contract-dependent businesses, regulated industries, businesses with critical licenses |

| Common Industries | Retail, e-commerce, contracting, manufacturing | Healthcare, franchises, SaaS, financial services, skilled trades, government contracting |

| Hybrid Option Available? | No — structure is already asset-based | Yes — can elect Section 338(h)(10) for asset-sale tax treatment |

| Administrative Burden | Higher; requires new bank accounts, payroll, vendor accounts | Lower; existing accounts and systems continue |

| Negotiation Dynamics | Buyers prefer asset sales | Sellers prefer stock sales |

How a Business Broker Helps You Choose the Right Structure

A seasoned broker helps you navigate the complexities by:

- Modeling tax outcomes under both structures

- Identifying potential liability risks

- Assessing the impact on financing and buyer pool

- Coordinating with attorneys and CPAs

- Negotiating structure adjustments to maximize your net proceeds

- Anticipating red flags that could delay closing

The right structure is rarely chosen at random — it’s the result of financial modeling, negotiation leverage, tax planning, and industry-specific considerations. With the proper guidance, sellers can strategically position the deal to attract strong buyers and maximize earnings.

Consult a Business Broker to Sell Your Business

Choosing between an asset sale and a stock sale is one of the most critical decisions in any business transaction. While the end goal is the same — transferring ownership — the structure you choose shapes everything that happens before, during, and after the sale. Taxes, liabilities, buyer risk, seller payout, regulatory hurdles, and the overall ease of transition all hinge on whether the deal is structured as an asset transfer, a stock purchase, or a hybrid election under Section 338(h)(10).

For most buyers, asset sales offer cleaner protection and better tax benefits. For most sellers, stock sales provide simpler exits and more favorable capital gains treatment. And for those situations where both sides want different advantages, strategic tools like Section 338(h)(10) can create a negotiated middle ground that satisfies everyone involved.

Because no two businesses are identical, the “best” structure is highly situational — driven by the company’s industry, asset mix, contracts, licenses, liabilities, and long-term goals of both parties. That’s why successful business sales require more than just a willing buyer and seller. They require thoughtful planning, sophisticated tax modeling, careful due diligence, and deal experience.

A skilled business broker brings all of this together. By coordinating with CPAs, attorneys, lenders, and both sides of the transaction, a broker ensures the sale structure is optimized, risks are managed, and the seller walks away with the strongest possible financial outcome. With the right strategy and the right professionals guiding the process, business owners can confidently choose the structure that protects their interests and maximizes the value of their life’s work.

Consult an expert today.