For aspiring entrepreneurs and investors, the question often arises: Is it better to start a business from scratch or buy an existing one?

While entrepreneurship is commonly associated with launching a new venture, buying an established business has become an increasingly popular alternative. From small local enterprises to large acquisitions backed by private equity, business purchases occur across every industry and economic cycle.

Buying a business can offer speed, stability, and proven performance—but it also comes with risks, complexity, and significant financial commitment. Whether purchasing a business is a good idea depends on the buyer’s goals, experience, risk tolerance, and ability to execute a successful transition.

This article explores the advantages, disadvantages, risks, financial considerations, and strategic factors involved in buying a business, helping readers make a more informed decision.

Understanding What It Means to Buy a Business

Buying a business involves acquiring ownership of an existing company, either through purchasing its assets or buying its shares or membership interests. Unlike starting a business, the buyer steps into an operation that already has customers, employees, systems, and a track record.

Businesses can be purchased from retiring owners, entrepreneurs seeking new opportunities, family businesses without successors, or investors exiting for strategic reasons. Buyers may be individuals, partnerships, strategic companies, or financial investors.

The appeal lies in acquiring something that already works—but that does not mean success is guaranteed.

The Case for Buying a Business

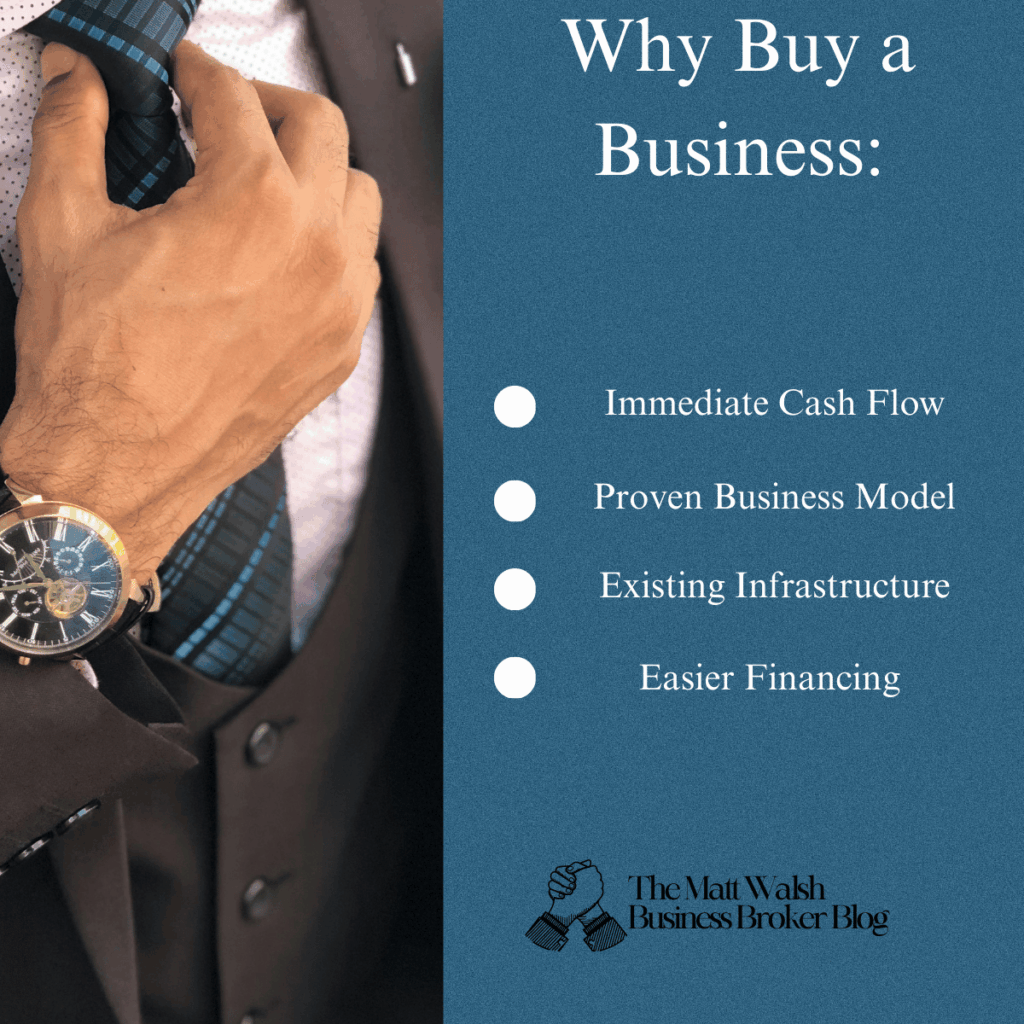

1. Immediate Cash Flow

One of the strongest arguments in favor of buying a business is immediate revenue and cash flow. Unlike startups, which may take years to become profitable, an established business is already generating income. This allows buyers to:

- Pay themselves a salary sooner

- Service acquisition debt

- Reinvest in growth

For buyers relying on financing, cash flow is often essential to making the deal viable.

2. Proven Business Model

An existing business has already demonstrated that its product or service has market demand. This significantly reduces one of the biggest risks faced by startups: uncertainty about whether customers will buy.

A proven model provides insight into:

- Pricing strategies

- Cost structure

- Customer behavior

- Market positioning

Rather than experimenting from scratch, buyers can focus on improving and scaling what already works.

3. Established Brand and Customer Base

Most established businesses come with brand recognition, customer relationships, and goodwill. These intangible assets can take years to build organically.

Benefits include:

- Repeat customers

- Existing contracts or subscriptions

- Word-of-mouth reputation

- Market credibility

This foundation can provide stability and a competitive advantage, especially in crowded markets.

4. Existing Infrastructure and Workforce

Buying a business often means acquiring trained employees, operational systems, supplier relationships, and technology. This infrastructure allows the buyer to focus on leadership and strategy rather than building everything from the ground up.

Key advantages include:

- Experienced staff who understand daily operations

- Established vendor and supplier networks

- Operational processes already in place

This reduces the learning curve and operational risk.

5. Easier Access to Financing

Lenders are generally more comfortable financing acquisitions of established businesses than startups. Historical financial performance provides lenders with data to assess risk, making loans more attainable.

Financing options may include:

- Bank loans

- SBA-backed loans

- Seller financing

- Private investors

This accessibility can make buying a business more feasible than starting one without capital.

The Risks and Challenges of Buying a Business

Despite the advantages, buying a business is not without significant risks.

1. High Upfront Cost

Purchasing a business often requires substantial capital, including:

- Purchase price

- Legal and advisory fees

- Working capital

- Transition costs

Even with financing, buyers typically need a meaningful equity contribution. This financial commitment increases risk if the business underperforms.

2. Hidden Problems and Liabilities

Not all issues are visible at first glance. A business may appear profitable while hiding problems such as:

- Declining customer loyalty

- Outdated technology

- Regulatory non-compliance

- Pending legal disputes

- Overdependence on the previous owner

Thorough due diligence reduces risk, but it cannot eliminate uncertainty entirely.

3. Transition and Integration Challenges

Ownership changes can disrupt operations. Employees, customers, and suppliers may feel uncertain, leading to turnover or lost business.

Common challenges include:

- Employee resistance to new leadership

- Cultural misalignment

- Loss of key customers

- Knowledge gaps after the seller exits

A poorly managed transition can erode value quickly.

4. Overreliance on the Seller

Some businesses depend heavily on the owner’s personal relationships, expertise, or reputation. If customers associate the business primarily with the seller, retaining value after the sale can be difficult.

Buyers must assess whether the business can operate independently of its previous owner.

5. Limited Growth Potential

Not every business has strong growth prospects. Some may be stable but mature, operating in declining industries or saturated markets.

Without clear opportunities for improvement or expansion, buyers may struggle to increase value or justify the purchase price.

Financial Considerations When Buying a Business

Buying a business is not only an entrepreneurial move but also a significant financial investment. Careful evaluation of valuation, financing, and expected returns is essential to ensure the purchase aligns with long-term financial goals.

Valuation and Pricing

Determining whether a business represents good value begins with proper valuation. Buyers commonly rely on several methods to assess a fair purchase price. Earnings multiples, such as EBITDA, are frequently used to estimate value based on profitability. Cash flow analysis focuses on the business’s ability to generate consistent income, while asset-based valuation considers the worth of tangible and intangible assets. Comparable sales provide additional context by examining prices paid for similar businesses in the market.

Regardless of the method used, overpaying can significantly reduce future returns and increase financial risk. Even a well-run business can become a poor investment if the purchase price leaves little room for growth or error. Sound valuation protects buyers from unrealistic expectations and helps establish a solid foundation for future performance.

Financing Structure

The way a business is financed has a direct impact on both risk and reward. Buyers must carefully examine debt levels and repayment obligations, as excessive debt can strain cash flow and reduce operational flexibility. Interest rates and loan covenants also matter, as restrictive terms may limit decision-making.

Seller financing can be an attractive option, often signaling seller confidence while reducing the buyer’s upfront cash requirement. Earn-outs or deferred payments may also be used to bridge valuation gaps, tying part of the purchase price to future performance. However, excessive leverage can magnify financial pressure and limit the ability to reinvest in growth.

Return on Investment

Ultimately, buyers should assess whether the expected return justifies the risk and effort involved. This includes evaluating cash flow yield, long-term appreciation potential, and realistic exit opportunities. Buying a business is not just about ownership—it is a disciplined investment decision that requires financial clarity and strategic planning.

Buying vs. Starting a Business

Choosing between buying an existing business and starting one from scratch is a major entrepreneurial decision. Each option offers distinct advantages and challenges, and understanding these trade-offs can help align your choice with your goals, resources, and risk tolerance.

Buying a Business: Stability and Speed

Buying an established business often provides a faster route to cash flow. Because the business is already operating, it typically has existing customers, suppliers, and revenue streams in place. This reduces the uncertainty associated with market demand and allows the new owner to focus on improving or scaling operations rather than building them from the ground up.

Another key benefit is proven operations. Systems, processes, and staff are usually already established, which can make day-to-day management more predictable. However, these advantages come at a cost. Purchasing a business usually requires a higher upfront investment, and financing may be necessary. Additionally, while market risk is generally lower, buyers often have less creative freedom, as they inherit the brand, culture, and operational structure of the existing business.

Starting a Business: Freedom and Opportunity

Starting a business from scratch typically involves a lower initial financial outlay, making it more accessible for first-time entrepreneurs. One of the biggest advantages is full creative control. Entrepreneurs can shape the brand, products, and culture according to their vision, without being constrained by existing practices.

However, this freedom comes with greater risk. New businesses face a higher likelihood of failure due to unproven ideas, limited resources, and uncertain customer demand. Building a customer base and achieving profitability often takes time, requiring patience, persistence, and careful financial management.

Choosing the Right Path

Neither buying nor starting a business is inherently better. The right choice depends on an individual’s objectives, risk tolerance, financial capacity, and desire for control. Understanding these factors is essential to making a decision that aligns with both personal strengths and long-term goals.

Who Should Consider Buying a Business?

Buying a business may be a good idea for:

- Professionals seeking entrepreneurship with reduced risk

- Investors looking for stable cash flow

- Executives transitioning from corporate roles

- Families seeking long-term income assets

- Entrepreneurs with operational experience

It may be less suitable for those with limited capital, low risk tolerance, or a strong desire to build something entirely new.

Industries Where Buying a Business Works Well

Certain industries are particularly well-suited to acquisitions, including:

- Professional services

- Healthcare practices

- Manufacturing

- Distribution and logistics

- Franchises

- Business-to-business services

These sectors often feature recurring revenue, established demand, and transferable operations.

The Importance of Due Diligence

Due diligence is the process of verifying information and identifying risks before completing a purchase. It typically covers:

- Financial records

- Legal compliance

- Customer and supplier contracts

- Employee agreements

- Operational processes

- Market conditions

Skipping or rushing due diligence is one of the most common and costly mistakes buyers make.

The Role of Professional Advisors

Buying a business is a complex process that involves legal, financial, and strategic considerations, making professional guidance essential for most buyers. Experienced advisors bring specialized knowledge that helps navigate each stage of the acquisition and reduces the risk of costly errors. Business brokers or M&A advisors play a key role in identifying suitable opportunities, valuing businesses, and facilitating negotiations between buyers and sellers. Their market insight can help buyers assess whether a deal is realistically priced and strategically sound.

Attorneys are critical for managing legal risks, reviewing contracts, and ensuring that transaction documents accurately reflect agreed-upon terms. Accountants and tax specialists analyze financial statements, evaluate cash flow, and help structure the transaction in a tax-efficient manner. Lenders and financial planners assist buyers in securing appropriate financing and assessing how the acquisition fits into broader financial goals.

Together, these professionals provide objective advice, coordinate complex details, and support informed decision-making. Experienced advisors help buyers avoid common pitfalls, negotiate more effectively, and structure deals that align with both short-term feasibility and long-term success. Engaging the right advisory team significantly improves the likelihood of completing a successful acquisition and realizing the full potential of the investment.

Post-Purchase Success Factors

Purchasing a business marks the start of a new phase rather than the finish line. Long-term success depends on how effectively the buyer manages the transition and leads the business forward. Strong leadership and clear communication are essential in establishing trust with employees, customers, and partners. New owners who communicate their vision while listening to concerns are more likely to gain support and maintain stability.

Retaining key employees is another critical factor. Experienced team members carry institutional knowledge and relationships that help ensure continuity. Creating incentives, offering reassurance, and demonstrating respect for existing roles can reduce turnover during the transition period. Maintaining customer trust is equally important, as customers may feel uncertain about changes in ownership. Consistent service quality and proactive communication help preserve loyalty.

Successful buyers also understand the value of making gradual, thoughtful changes rather than sweeping reforms. Taking time to understand operations allows improvements to be implemented strategically without disrupting performance. Finally, a clear and realistic growth strategy provides direction and purpose. Buyers who build on what already works while carefully enhancing operations are far more likely to achieve sustainable success and long-term value creation.

When Buying a Business May Not Be a Good Idea

While buying a business can be a powerful path to ownership and wealth creation, it is not always the right decision. Certain warning signs should prompt buyers to proceed with caution or reconsider the opportunity altogether. One major concern arises when financial records are unreliable, incomplete, or inconsistent. Without accurate financial information, it becomes difficult to assess true profitability, cash flow, and risk, increasing the likelihood of unpleasant surprises after the purchase.

Industry conditions also matter. Businesses operating in sectors experiencing steep or long-term decline may struggle to maintain revenue, regardless of how well they are managed. Similarly, a price that is not supported by actual cash flow can create financial strain, especially when debt is used to finance the acquisition.

Buyer readiness is equally important. Individuals who lack operational or leadership experience may find it challenging to manage employees, systems, and daily responsibilities. In addition, buyers who expect a business to function as a passive investment often underestimate the level of involvement required. Most small and mid-sized businesses demand active management, particularly during the transition period.

Recognizing these red flags early helps buyers avoid costly mistakes, protect capital, and focus on opportunities that align with their skills, expectations, and long-term goals.

Long-Term Wealth and Exit Considerations

When buying a business, it is essential to think beyond the initial acquisition and consider the long-term wealth and exit implications. A successful purchase is not only about generating income today but also about preserving and enhancing value for the future. Buyers should evaluate the business with an eventual exit in mind, even if they plan to own it for many years.

One key question is whether the business can be sold again. A company with transferable systems, documented processes, and limited dependence on the owner is far more attractive to future buyers. Scalability is another important factor. Businesses that can grow through new markets, additional locations, or expanded product offerings often provide greater long-term value and flexibility.

Predictable and recurring earnings also play a critical role in wealth creation. Consistent cash flow supports financial stability during ownership and increases valuation at exit. Buyers should assess revenue diversity, customer retention, and margin sustainability to understand the reliability of future earnings.

A well-chosen acquisition can deliver ongoing income while also functioning as a valuable asset that can be sold, passed on, or leveraged in the future. By considering exit options early, buyers position themselves to build lasting wealth rather than simply purchasing a job.

Conclusion: Is Buying a Business a Good Idea?

Buying a business can be an excellent idea—but it is not the right choice for everyone. It offers immediate cash flow, proven operations, and reduced market risk compared to starting from scratch. However, it also requires significant capital, careful due diligence, and active involvement to manage risks and ensure a smooth transition.

Success depends on buying the right business at the right price, with a clear understanding of its strengths, weaknesses, and growth potential. For buyers who approach the process with discipline, realistic expectations, and professional support, purchasing a business can be a powerful path to entrepreneurship, financial independence, and long-term value creation.